Coinbase Commerce is changing, and for many merchants this is not a small dashboard update. It affects how crypto payments are created, where funds settle, which countries are eligible, what happens to old Commerce wallets, and whether an existing API or checkout flow can continue working after the deadline.

According to Coinbase Help, Coinbase Commerce is being unified with Coinbase Business. Merchants must complete the transition by March 31, 2026. After that date, the Commerce portal becomes inaccessible. Coinbase Business is currently available to businesses with a legal entity in the United States or Singapore, while merchants outside those regions need to move to an alternative provider if they want to keep accepting crypto payments.

That creates a very practical question: how should a merchant migrate without losing payment history, breaking checkout, confusing customers, or creating support problems?

This article is not a “top 10 gateways” list. It is a migration checklist for businesses that already understand why crypto payments matter, but now need to choose the next setup carefully.

What is actually changing with Coinbase Commerce

The important point is that Coinbase Commerce and Coinbase Business are not the same product under a new name. Coinbase describes the move as a shift from an older, self-custodial Commerce model toward a more stablecoin-first business platform with custody, offramps, accounting integrations, invoicing, and payments.

For some US and Singapore merchants, Coinbase Business may be the natural path. They can apply for Coinbase Business, update API integrations if needed, export Commerce transaction history, withdraw remaining funds from Commerce wallets, and begin using the new platform for payment links or invoicing.

For merchants outside the United States and Singapore, the situation is different. Coinbase says Coinbase Business is not yet available in those regions and that those businesses need to transition to an alternative provider before March 31, 2026 if they want to continue accepting crypto payments.

This distinction matters. A merchant should not evaluate alternatives only because “Coinbase Commerce is closing”. The real question is whether the new model fits the company’s region, payment flow, custody preference, assets, reporting, and operational process.

Do not migrate only by fee

The easiest comparison is the wrong one: transaction fee versus transaction fee. Fees matter, but they are not enough to choose a crypto payment provider.

A merchant moving from Coinbase Commerce should also look at the payment flow behind the fee. Does the provider support payment links, hosted checkout, API, invoices, or widgets? Can the team track payment statuses without manual wallet checks? How are underpayments and late payments handled? What happens when a customer sends the right asset on the wrong network? Can finance export the data it needs?

This is where a migration project becomes broader than a provider switch. If the old setup was mostly “create a charge and wait for crypto”, the new setup is a chance to improve the whole payment operation.

A useful starting point is to revisit what a crypto payment gateway for businesses actually does. The provider is not just a payment address. It sits between checkout, customer support, finance, settlement, refunds, and internal order logic.

Export history before it becomes a problem

Before touching checkout, merchants should preserve records. Coinbase specifically tells Commerce users to export transaction history before March 31, 2026. That history may be needed for accounting, refunds, customer disputes, tax records, or internal reconciliation.

This is especially important because Commerce and Coinbase Business are separate systems. Coinbase says Commerce transaction history does not transfer automatically to Coinbase Business. Even if a business later chooses Coinbase Business or another provider, old payment data still belongs in internal records.

For merchants migrating to an alternative provider, the same principle applies. Do not treat payment history as something the old dashboard will always keep available. Export reports, transaction records, wallet data, customer references, invoice IDs, and any support-relevant details while the portal is still accessible.

The migration should leave the company with a clean archive of old payments and a clean starting point for new payments.

Check what happens to old wallet funds

The wallet question is easy to underestimate. Coinbase Commerce wallets are self-custodial, and Coinbase notes that funds in a Commerce wallet must be withdrawn before March 31, 2026. After that date, the Commerce withdrawal tool is disabled.

This is not just a finance task. It can involve seed phrase access, destination wallet choice, network fees, operational approval, and internal records. If several people managed the old Commerce setup over time, the business may need to confirm who still has access, where backups are stored, and what balances remain.

A safe migration should separate two workstreams: closing the old setup and launching the new one. The old setup needs exports, wallet withdrawals, and a plan for open invoices. The new setup needs checkout configuration, payment testing, support scripts, and finance reporting.

If these tasks are mixed together at the last minute, the business risks losing visibility over both.

API merchants need more than a new endpoint

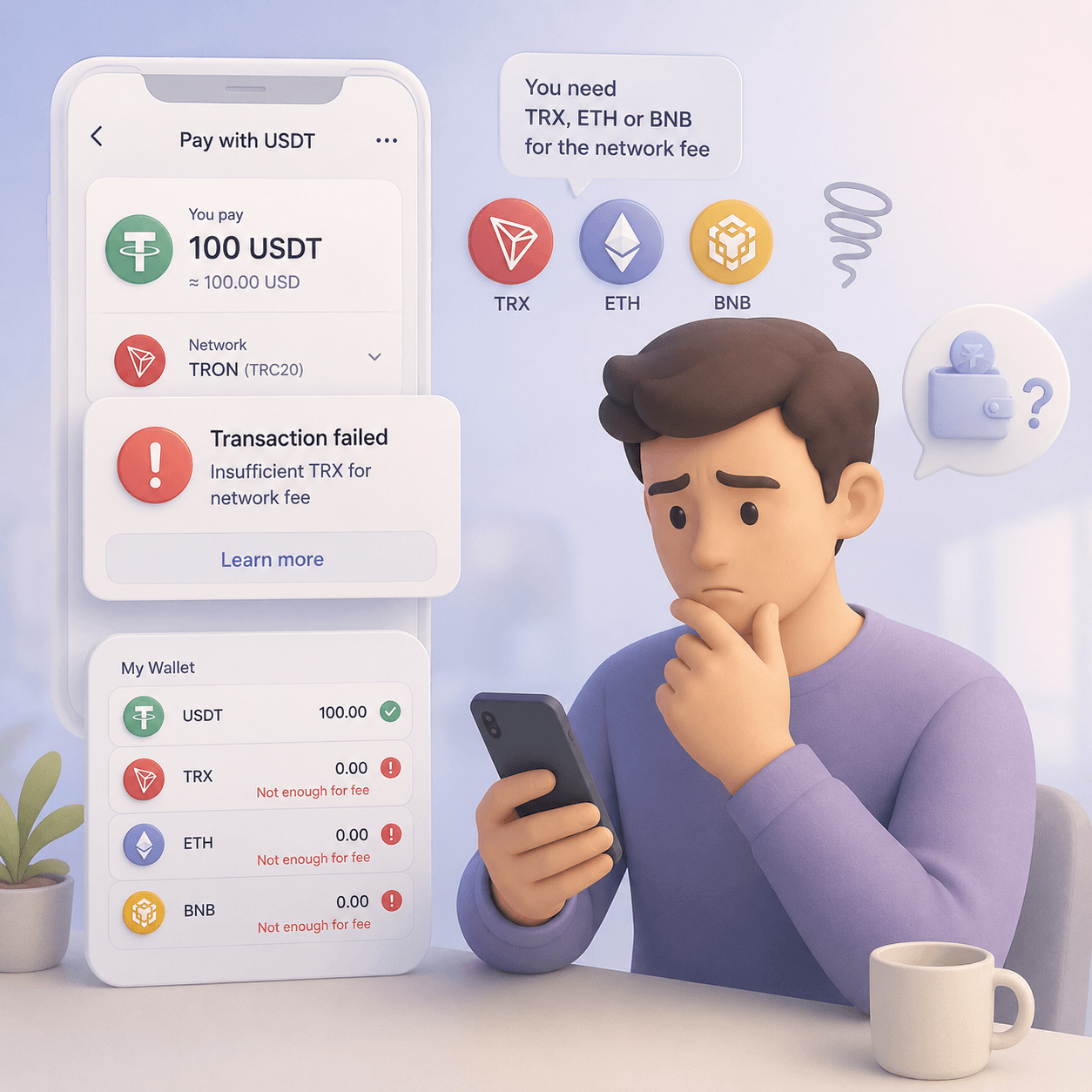

Merchants that used Coinbase Commerce through a dashboard can often migrate by replacing payment links or invoices. API-based merchants have a deeper job. They need to understand request and response changes, authentication, payment status logic, webhook behavior, order matching, and sandbox or low-risk testing.

The business impact can be larger than the engineering task suggests. If payment statuses change, the product may credit orders too early or too late. If webhook handling is incomplete, support may see paid customers whose orders remain pending. If the new provider has different expiration rules, the checkout UX may change.

Before choosing an alternative, developers and product teams should review the same questions they would ask when choosing any crypto payment API: how invoices are created, how statuses are updated, how webhooks are verified, how underpayments are handled, and how the payment connects to the internal order.

A migration is a good moment to remove old assumptions. Do not rebuild the same fragile flow with a different provider name.

Payment links, widgets, invoices, or API

Not every merchant needs the same replacement setup. Some companies used Coinbase Commerce for simple payment links. Others embedded crypto checkout into a product, app, SaaS flow, or digital goods delivery process.

A small service business may be fine with payment links or invoices. An online store may need a hosted checkout or plugin-like flow. A SaaS, marketplace, or digital product platform may need API logic that connects payment status to access, balance, subscription, or license delivery. A team that wants to test crypto payments before a full integration may start with crypto payment links and QR invoices, then move to API later.

The point is not to choose the most technical option. The point is to choose the option that matches how the business sells.

A provider with payment links but weak API support may fit manual invoicing and fail for product-led checkout. A provider with API but poor support workflows may create unnecessary tickets. A provider with many assets but unclear network logic may increase wrong-network payments. The migration should match the actual payment journey.

Refunds and customer support should be part of the plan

Many merchants treat refunds as a future problem. During migration, that is risky. Old invoices may still be open. Customers may pay late. Some may send funds to an old address. Others may ask about a transaction created before the switch.

Crypto refunds already require clearer rules than card refunds. Transactions are usually irreversible, amounts can differ from invoices, and network fees matter. During migration, the support team also has to know whether a payment belongs to the old provider or the new one.

Before switching providers, write a simple internal policy for edge cases: late payment, underpayment, overpayment, wrong network, old invoice, duplicate payment, and customer request for refund. The existing guide to crypto payment refunds can help structure those cases.

This is not only about protecting the business. It also prevents customers from receiving inconsistent answers during a sensitive transition.

Settlement, off-ramp, and reporting

One of the reasons Coinbase gives for the Commerce transition is that business expectations have changed. Merchants now want custody, compliance, offramps, accounting tools, and operational tooling. That is a useful signal for anyone choosing an alternative.

A merchant should ask where funds go after a customer pays. Do they remain in a wallet controlled by the business? Are they converted to stablecoins? Can they be withdrawn manually or automatically? Is there fiat settlement? What records can finance export? Which team members can access the dashboard?

If the business accepts USDT or other stablecoins, settlement is not just an accounting detail. It affects volatility, cash flow, withdrawal timing, and reporting. The newer guide to crypto on-ramp and off-ramp for business is useful here because migration is not only about replacing checkout. It is also about deciding how crypto becomes usable business money.

Where CryptumPay can fit

CryptumPay can be relevant for businesses that want a crypto payment setup around USDT, popular networks, payment statuses, payment links or QR invoices, API or widget integration, dashboard history, AML checks, and controlled operations.

That does not mean every Coinbase Commerce merchant should choose the same replacement. A US or Singapore business may decide that Coinbase Business fits its needs. A company that wants a custodial, stablecoin-first platform may prefer one type of provider. A merchant that wants a different asset mix, region availability, checkout model, or operational flow may look elsewhere.

The practical way to evaluate CryptumPay is not “is it a Coinbase clone?” It is “does it support the way this business wants to accept, track, reconcile, and withdraw crypto payments?”

If a merchant needs to keep accepting crypto while avoiding a rushed migration, the right next step is to map its current Commerce usage against the new provider’s payment flow: payment creation, customer UX, status handling, refunds, finance records, and settlement.

A practical migration sequence

A smooth migration usually starts before the technical switch. First, confirm whether the business is eligible for Coinbase Business or needs an alternative provider. Then export Commerce history and withdraw funds while access is still available. After that, map the current payment flow: dashboard charges, payment links, API, invoices, open orders, refunds, and support cases.

Only then should the team configure the new provider and test real payment scenarios. The test should include a normal payment, a delayed payment, an underpayment, a wrong-network attempt if relevant, a refund scenario, and finance export. Once the new flow works, replace old payment links, stop creating new Commerce charges, update customer-facing payment instructions, and monitor support tickets during the first days after launch.

The goal is not just to “move before March 31”. The goal is to avoid a broken checkout, missing records, stuck funds, and confused customers.

Conclusion

Coinbase Commerce migration is not just a provider replacement. It is a chance to rethink how crypto payments should work for the business in 2026.

Some merchants will move to Coinbase Business. Others need an alternative because of region, custody preference, asset support, checkout flow, API requirements, or operational needs. In both cases, the migration should be handled as a payment operations project, not a quick settings change.

The safest approach is to protect old records, withdraw old funds, choose the right checkout model, test status logic, prepare support, and make sure finance can reconcile new payments from day one. That is what turns a forced migration into a cleaner crypto payment setup.