Crypto payment refunds are not just a customer support issue. They are part of payment operations.

When a customer pays by card, merchants are used to a familiar set of actions: authorize, capture, void, refund, dispute, chargeback. Crypto payments work differently. Once a blockchain transaction is confirmed, the original transaction cannot simply be rolled back. A refund usually becomes a new transaction, a customer credit, a balance adjustment, or a manual exception linked to the original order.

That difference matters for any business accepting USDT, BTC, ETH or other crypto assets on a website, in an app, through a payment link, in Telegram, or inside a digital platform. If a customer sends too little, sends too much, chooses the wrong network, pays after the invoice expires, or sends funds without the required memo, the business needs a clear process.

Without that process, crypto payments may still work — but every exception becomes a support ticket, a finance question, or a developer escalation.

This guide explains how businesses should handle crypto payment refunds, underpayments, overpayments and mistaken transfers without creating operational chaos.

Why crypto refunds are different from card refunds

A crypto refund is not the same as reversing a card payment.

In card payments, the payment system includes reversal and dispute mechanisms. In crypto, the blockchain transaction is final once confirmed. The merchant can still return value to the customer, but that return is a separate operation.

That changes the merchant’s responsibility. The business needs to know:

- which order the payment belongs to;

- which asset was expected;

- which network was used;

- how much was expected;

- how much was actually received;

- whether the invoice was still valid;

- whether the transaction passed risk checks;

- whether the customer should receive a refund, a credit, a top-up, or a request to pay the remaining amount.

This is why accepting crypto through a simple wallet address is risky for a growing business. It may work for occasional manual payments, but it does not give support, finance and product teams enough structure when something goes wrong.

If your team already sees many payment errors before funds arrive, start with the broader guide to failed crypto payments. Refunds are often the next stage of the same problem: the customer has sent money, but the payment does not match the order cleanly.

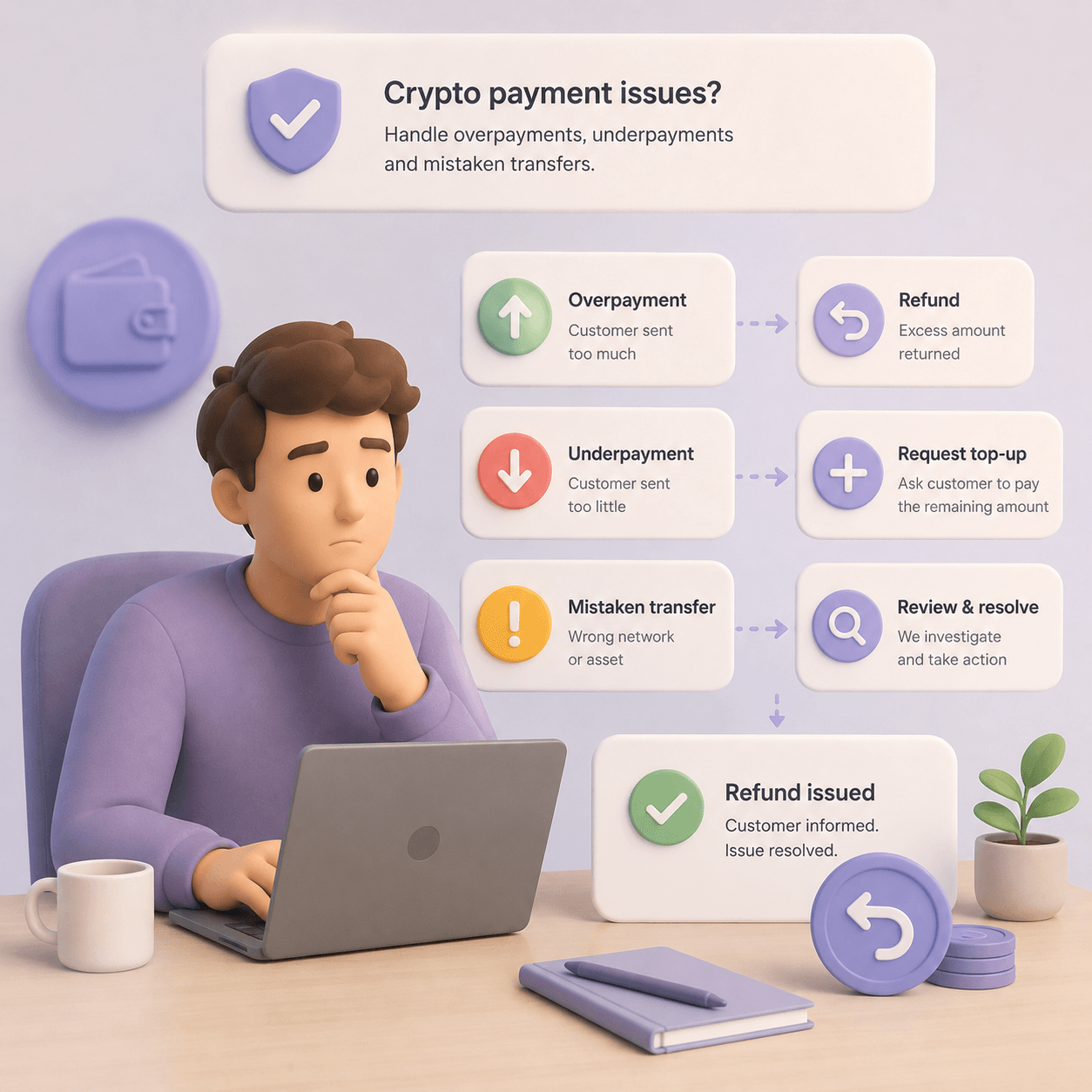

The main refund and exception scenarios

Most crypto refund cases fall into a few categories. They may look similar to the customer — “I paid, where is my order?” — but they need different handling inside the business.

Common scenarios include:

- the customer sends less than the required amount;

- the customer sends more than the required amount;

- the customer pays after the invoice expires;

- the customer sends the right asset on the wrong network;

- the customer sends an unsupported asset;

- the customer pays twice;

- the customer sends funds without memo, tag or another required identifier;

- the payment arrives but cannot be matched to an order;

- the transaction is held for risk or AML review;

- the customer requests a normal commercial refund after purchase.

Treating all of these as “refunds” is too broad. A good payment operation separates them into statuses and rules.

For example, an underpayment may require a top-up. An overpayment may require a partial refund. A wrong-network transfer may require manual investigation. A late payment may be accepted if it arrived shortly after expiry, but rejected if pricing or inventory changed. A suspicious transaction may need compliance review before any funds move out.

Underpayments: ask for more, accept partially, or refund

An underpayment happens when the customer sends less than the invoice requires.

Example: the invoice asks for 100 USDT, but the business receives 99.40 USDT. This can happen because the customer changed the amount manually, misunderstood network fees, paid from an exchange that deducted a fee, copied the wrong amount, or tried to round the payment.

From the customer’s perspective, the difference may look small. From the business perspective, it can affect revenue recognition, access delivery, inventory, subscriptions and support.

There are three practical ways to handle underpayments.

Ask the customer to pay the remaining amount

This is usually the right option for fixed-price purchases.

If a customer buys a one-year subscription, a digital product, a course, a license, a physical product or a B2B invoice, the business may not want to deliver the order until the full amount is received.

The payment page and support team should clearly show:

- expected amount;

- received amount;

- remaining amount;

- asset and network;

- original invoice ID;

- deadline for the remaining payment;

- what happens if the customer does not pay the rest.

The key is to connect the second transaction to the same order. If the customer pays the remainder but your backend treats it as a separate unknown payment, support will still need to investigate manually.

This is where the crypto payment API matters. Your integration should support clear invoice IDs, statuses, webhooks, transaction hashes, order metadata and idempotent crediting logic.

Accept the underpayment within a threshold

Some businesses choose to accept small underpayments. This can make sense when the shortfall is tiny and the cost of manual support is higher than the missing amount.

For example, a business may decide that underpayments within 0.5% or 1% can be accepted for some products. That rule should not be emotional. It should depend on margin, payment size, product type and customer experience.

A practical threshold policy might separate cases like this:

- small underpayment on a high-margin digital product: accept;

- underpayment on a low-margin physical product: ask for the remainder;

- underpayment on an internal balance top-up: credit the actual received amount;

- underpayment on a subscription renewal: keep the renewal pending until completed;

- underpayment on a B2B invoice: route to finance review.

The important distinction is fixed-price order versus balance model.

If a customer is buying a specific product, the order usually requires exact payment. If the customer is topping up an internal balance in a hosting, iGaming, ad network, API, VPN or SaaS product, the business may simply credit what arrived.

Refund the underpayment

A refund may be the right option if the customer does not want to pay the remainder, the product cannot be delivered for a lower amount, or the invoice is no longer valid.

But refunding an underpayment is not free. It can involve a network fee, a minimum refund threshold, a supported network, customer address verification and internal approval.

Before refunding, check:

- whether the refund amount is large enough after network fees;

- whether the refund should go to the original address or a new address;

- whether the customer paid from an exchange;

- whether the network is supported for refunds;

- whether the transaction needs AML review;

- how the refund will appear in finance reports.

Small underpayments can be especially awkward. If the amount is lower than the network cost of refunding, the business needs a policy: customer credit, balance, coupon, manual settlement, or no refund below a stated threshold where legally permitted.

Overpayments: refund the excess or credit the balance

An overpayment happens when the customer sends more than the invoice requires.

This is easier to complete than an underpayment because the business received enough to cover the order. But the extra amount still needs a decision.

Overpayments often happen because customers pay manually, round up, pay from an exchange, copy a stale amount, or send extra funds “just in case” to cover fees. That habit creates accounting and support issues.

There are two main approaches.

Refund the excess amount

For fixed-price purchases, the cleanest option is usually to complete the order and refund the overpaid portion.

This works for:

- e-commerce orders;

- digital downloads;

- licenses;

- course purchases;

- one-time SaaS plans;

- B2B invoices;

- paid access products.

The customer should see that the order was paid successfully and that the extra amount is being refunded, waiting for claim, or being reviewed.

The refund communication should explain:

- original invoice amount;

- received amount;

- overpaid amount;

- network used;

- network fee policy;

- expected refund status;

- whether the refund is automatic or manual.

Credit the excess to the customer balance

For balance-based products, refunding the excess may be unnecessary. If the customer is topping up an account, the extra amount can become additional balance.

This is often better for:

- iGaming deposits;

- ad network balances;

- hosting and VPS credits;

- API credits;

- marketplace wallets;

- paid communities;

- usage-based SaaS.

But the customer should not be left guessing. The account should clearly show that the order was completed and the excess was credited.

If your business sees frequent overpayments, review the payment UX. Customers may be changing the amount manually because the checkout does not clearly explain crypto payment fees, network costs or the difference between the invoice amount and wallet fee.

Wrong network transfers: the hardest support case

Wrong-network payments are among the most difficult crypto payment exceptions.

A customer may think “USDT is USDT,” but USDT on TRON, Ethereum, BNB Smart Chain, Polygon and Solana are different payment routes. If the invoice expects USDT on TRON and the customer sends USDT on another network, the result depends on address control, provider support, asset support and recovery rules.

The business should not promise that every wrong-network payment can be recovered. Sometimes it can be handled manually. Sometimes the funds may be technically visible but not recoverable through the payment flow. Sometimes recovery is not supported or not worth the cost.

A proper wrong-network process should collect:

- original invoice ID;

- expected asset;

- expected network;

- actual network used;

- transaction hash;

- destination address;

- amount sent;

- customer account ID;

- time of payment;

- risk review status.

Then the business can decide whether to refund, credit, recover manually, escalate, or reject the case.

The best way to reduce wrong-network tickets is to make network choice clear before payment. Do not show a long list of networks without context. Explain which network the customer selected, what asset format is expected, and what happens if they use another network.

For more detail, use the guide on choosing a USDT network.

Late payments after invoice expiry

Crypto invoices often expire. This protects the business from price changes, stale quotes, inventory changes and old payment links.

But customers do not always behave within the timer. They may open the payment page, get interrupted, return later and send the funds anyway. Or they may send the payment before the timer ends, but the transaction confirms after the invoice expires.

A late payment needs a business rule.

Possible actions include:

- accept it if the amount is correct and the delay is small;

- ask for an additional amount if pricing changed;

- refund it if the order is no longer valid;

- credit the amount to the customer’s internal balance;

- route it to manual review if it cannot be matched.

The right answer depends on the business model.

For a digital product with stable pricing, accepting a slightly late payment may preserve revenue and reduce support frustration. For a volatile quote, limited inventory, marketplace order or B2B invoice, late payment may require finance approval.

The payment page should not simply show “expired” and leave the customer confused. It should explain what to do if the customer has already sent funds: provide the transaction hash, wait for detection, contact support, or follow an automated resolution flow.

Unsupported assets, missing memo and destination tags

Some crypto payment errors are not about amount. They are about identification.

A customer may send the wrong asset to the right network. Or they may forget memo, tag, destination tag or another identifier required to match the transaction to their account.

This is common in payment flows involving assets or platforms that rely on additional identifiers. If that identifier is missing, funds may arrive but cannot be automatically assigned to the correct customer.

Support should not resolve these cases from screenshots alone. The team needs transaction-level data.

Required information should include:

- transaction hash;

- asset;

- network;

- destination address;

- memo or tag, if any;

- expected invoice or order ID;

- customer ID;

- amount;

- timestamp.

If memo or tag is required, the payment page must make it obvious. Do not hide it in small text. Customers should understand that address, amount and memo/tag may all be required for the payment to be credited correctly.

Who pays the refund network fee?

A crypto refund is usually a new outbound transaction. That means network fees may apply.

There are several possible policies:

- the merchant refunds the full amount and absorbs the fee;

- the fee is deducted from the refund amount;

- the customer pays the fee separately;

- small refunds below a threshold are credited internally instead of sent on-chain;

- the business issues a coupon or account credit where appropriate.

There is no universal answer. A SaaS product with high customer lifetime value may choose to absorb small refund fees. A low-margin marketplace may need to deduct them. A balance-based platform may avoid on-chain refunds by crediting the customer account.

The important point is clarity. Customers should not discover the fee policy only after something goes wrong.

A refund policy should say:

- whether network fees are deducted;

- which network is used for refunds;

- whether refunds can be issued in another asset;

- whether there is a minimum refund amount;

- whether the customer must provide a refund address;

- whether the refund goes to the original address or a confirmed address;

- how long review usually takes.

What support needs to resolve crypto refund tickets

Crypto payment support should be data-driven. A screenshot from a wallet can help, but it should not be the source of truth.

Support agents need access to:

- order ID;

- invoice ID;

- customer account ID;

- expected amount;

- received amount;

- asset;

- network;

- destination address;

- transaction hash;

- invoice creation time;

- invoice expiry time;

- confirmation status;

- current payment status;

- exception reason;

- refund status;

- risk review status.

If first-line support cannot see this data, every refund case becomes an escalation to finance or engineering. That may be acceptable during a pilot, but it will not scale.

The business should also track exception categories. A high number of wrong-network tickets means the checkout needs better network guidance. Frequent underpayments may point to network fee confusion. Many expired-invoice tickets may mean the payment timer is too short or not visible enough.

The article on crypto payment metrics gives a broader framework for tracking support load, exception rate, time to credit and payment success rate.

What finance needs for reconciliation

Finance should not treat crypto refunds as informal wallet movements. Each refund should be tied to the original order and reflected in reporting.

A finance-ready crypto refund process should record:

- original order amount;

- expected crypto amount;

- received crypto amount;

- underpaid or overpaid difference;

- asset and network;

- exchange rate used for the invoice;

- provider fee;

- network fee;

- refund amount;

- refund asset and network;

- date of payment;

- date of refund;

- refund status;

- manual adjustments;

- AML or risk holds;

- final settlement amount.

This prevents a common reporting problem: counting an on-chain inflow as revenue even when it was underpaid, late, refunded or unmatched.

For USDT-heavy businesses, this connects directly to stablecoin payment operations for CFOs: reconciliation, settlement, conversion, withdrawals, fees and exception control.

What developers should build into the payment flow

Refunds and payment exceptions should not be bolted onto the system after launch. They should be part of the integration design.

At minimum, the backend should support clear payment states:

- created;

- waiting for payment;

- detected;

- confirming;

- completed;

- expired;

- underpaid;

- overpaid;

- late;

- wrong network;

- unsupported asset;

- unmatched;

- manual review;

- refund requested;

- refund processing;

- refunded;

- refund failed.

Product delivery should depend on business status, not merely on the existence of an on-chain transaction.

For example, a transaction may exist but still be underpaid. Another may be confirmed but linked to the wrong network. Another may be late and waiting for review. If the system grants access too early, the business creates its own loss.

Developers also need idempotency. Webhooks may arrive more than once. A payment can move from detected to confirming to completed. A refund can move from requested to processing to completed. The system must not credit the same balance twice or issue duplicate refunds.

How to reduce refunds before they happen

The best refund operation is one that prevents avoidable exceptions.

A strong crypto payment page should show:

- exact amount;

- asset;

- network;

- QR code;

- payment timer;

- instruction not to change the amount manually;

- network fee explanation;

- status after payment is sent;

- what happens if the invoice expires;

- what happens if the customer underpays;

- what support needs if something goes wrong.

Network-fee confusion is one of the most common causes of failed or partial payments. A customer may have enough USDT but not enough TRX, ETH, BNB, SOL or another native token to pay the network fee. That creates friction before payment and can also lead to incorrect amounts.

This is why gasless USDT payments are an important UX topic, not just a technical feature. If the payment flow can reduce native-token confusion, it can reduce underpayments and support tickets.

When AML review matters before a refund

A refund should not bypass risk controls.

If the incoming payment is suspicious, automatically sending funds out to a new address can create additional risk. This is especially important for larger amounts, high-risk industries, marketplaces, iGaming, anonymous accounts and cases where the customer asks to refund to an address different from the sending address.

AML or risk review may be needed when:

- the amount is large;

- the source wallet has risk signals;

- the customer requests a refund to a different address;

- the transaction is split into multiple transfers;

- the payment was sent through an unsupported route;

- the customer cannot prove a connection to the original payment;

- the payment came from a pooled exchange account;

- the transaction is already under review.

Requirements depend on jurisdiction, business model, transaction size and provider policy. This article is not legal advice. Operationally, the principle is simple: a crypto refund is also a financial transaction, so it should be tracked and controlled.

For a broader risk framework, read the guide to AML and crypto payment security.

What a crypto refund policy should include

A refund policy for crypto payments should be specific. Generic language like “refunds are processed where applicable” is not enough.

A practical policy should explain:

- supported assets and networks;

- what happens if the customer uses the wrong network;

- what counts as underpayment;

- whether small underpayments can be accepted;

- how overpayments are handled;

- whether excess funds are refunded or credited;

- how late payments are handled;

- who pays network fees;

- whether minimum refund amounts apply;

- which data the customer must provide;

- whether additional verification may be required;

- how long review may take;

- whether refunds are full, partial, or balance credits;

- whether commercial refunds differ from payment-error refunds.

Do not promise universal recovery of mistaken transfers. Do not promise instant refunds on every network. Do not promise that unsupported assets can always be returned. Clear limitations are better than vague optimism.

How CryptumPay fits into this workflow

CryptumPay is relevant when a business needs more than a wallet address. It is designed for accepting crypto payments on a website, in an app, in Telegram or in another digital platform, with a structured payment flow rather than a loose manual transfer.

For refund and exception handling, the important parts are operational: invoice context, amount, network, payment history, dashboard visibility, API integration, HTML widget options, AML controls, withdrawals and USDT settlement logic.

The QR/app flow can reduce manual entry. Network-fee handling can reduce amount errors. Support for repeated payments can make top-ups and renewals less dependent on manual wallet actions. These details do not remove the need for a refund policy, but they reduce the number of avoidable cases and give teams better data when exceptions happen.

The goal is not to make crypto refunds identical to card refunds. The goal is to make them predictable, auditable and manageable.

Pre-launch checklist for crypto refunds

Before accepting real customer payments, test more than the happy path.

Run these scenarios:

- exact payment;

- small underpayment;

- large underpayment;

- overpayment;

- duplicate payment;

- payment after invoice expiry;

- payment detected but confirmation delayed;

- wrong network;

- unsupported asset;

- missing memo or tag;

- webhook retry;

- webhook failure;

- manual refund;

- refund to original address;

- refund to a new customer-provided address;

- AML hold;

- customer support lookup by transaction hash;

- finance reconciliation after refund.

For each scenario, answer three questions:

- What does the customer see?

- What does support see?

- What does finance see?

If any answer is unclear, the payment flow is not ready to scale.

FAQ

Can a crypto payment be reversed?

A confirmed blockchain transaction cannot be reversed like a card payment. A business can still refund the customer, but the refund is usually a new outbound transaction, a customer credit, or a manual adjustment linked to the original order.

What should a merchant do if a customer underpays?

The merchant should compare the expected and received amounts, check the network and invoice status, then apply a rule: ask for the remaining amount, accept the underpayment within a threshold, credit the actual amount to balance, or refund the payment.

What happens if a customer overpays?

For fixed-price orders, the business can complete the order and refund the excess. For balance-based products, the overpaid amount can be credited to the customer’s account if the policy allows it.

Can USDT sent on the wrong network be refunded?

Sometimes, but not always. It depends on the network, asset, address control, provider support, amount, fees and risk review. Businesses should avoid promising automatic recovery for wrong-network transfers.

Who pays the network fee for a crypto refund?

That depends on the merchant’s policy. The business may absorb the fee, deduct it from the refund, credit the customer internally, or apply a minimum refund threshold. The rule should be visible before customers pay.