Crypto payments for marketplaces are more complex than crypto payments for a single online store.

A store accepts money for its own product. A marketplace accepts money for products or services sold by many sellers, keeps a platform fee, updates seller balances, handles refunds, and pays sellers according to platform rules.

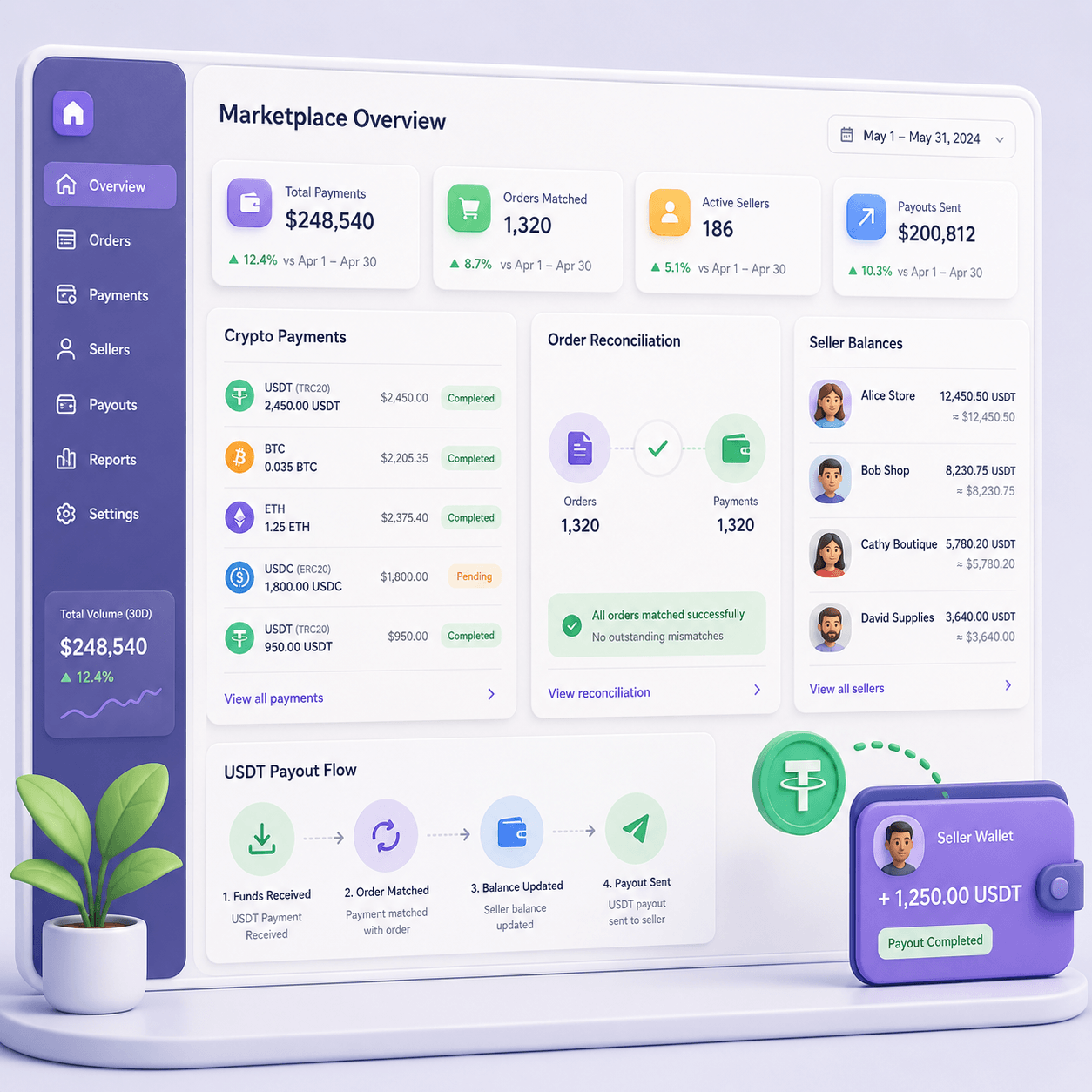

That means a simple “Pay with USDT” button is not enough. A buyer can pay, but the platform still needs to know which order the payment belongs to, which seller should receive the funds, how much commission the marketplace keeps, what fee was charged, whether the transaction passed risk checks, and when the seller can withdraw the money.

For a marketplace, crypto is not just another payment method. It becomes part of the operating system behind orders, seller balances, reconciliation, support, risk, and payouts.

Why marketplace crypto payments are different

In a standard e-commerce flow, the payment usually has one merchant and one order. The customer pays, the store receives the money, and the order moves to fulfillment.

In a marketplace, one payment can involve several parties:

- the buyer;

- one seller;

- multiple sellers in the same order;

- the marketplace;

- a payment provider;

- a logistics or service partner;

- the finance team;

- the support team;

- the risk or compliance team.

This changes the payment design. The marketplace has to answer operational questions before it launches crypto payments:

- Who receives the customer’s payment?

- When is an order considered paid?

- How is the platform commission calculated?

- When does the seller balance update?

- Who pays the blockchain network fee?

- What happens if the buyer underpays?

- What happens if the buyer sends funds on the wrong network?

- How are refunds handled?

- Can sellers withdraw in USDT or another asset?

- Which sellers need extra verification?

- What should the finance team reconcile every day?

A basic crypto payment gateway solves the first layer: accepting a crypto payment from a customer. A marketplace needs the next layer: connecting that payment to orders, sellers, commissions, balances, and payouts.

The three main payment models for marketplaces

Before choosing tools, define the money flow. The wrong model can make reconciliation painful later, even if the checkout works.

One platform account

In this model, all customer payments first go to the marketplace. The platform then calculates each seller’s share, keeps its commission, and pays sellers later.

This model is easier to start with because the platform controls the full payment flow. It works well for early-stage marketplaces, curated seller networks, digital product platforms, and B2B catalogs with a limited number of vendors.

The downside is operational responsibility. The marketplace must maintain accurate internal balances, seller statements, refund rules, reserves, and payout records. At low volume, this can be manageable. At high volume, manual spreadsheets and ad hoc wallet checks become a risk.

Split payments

Split payments distribute one customer payment between multiple parties. A marketplace might allocate part of the payment to the seller, part to the platform, and part to another partner.

With crypto payments, the split can happen in different ways. Some platforms may split funds at the infrastructure level. Others receive the payment centrally but record an internal split immediately: seller share, platform fee, reserve, and possible partner fee.

The benefit is transparency. Sellers can see exactly how their balance was calculated, and the platform does not need to manually rebuild every transaction after the fact.

The trade-off is complexity. Split logic must handle partial refunds, multi-seller orders, fee rounding, seller holds, risk reviews, and payout timing. It also needs a clear legal and compliance review, because requirements vary by jurisdiction and by the role the marketplace plays in the transaction.

Seller balances inside the platform

Many marketplaces do not pay sellers after every order. Instead, they maintain seller balances. Once an order is paid, the seller receives a balance entry. The funds may become available immediately, after delivery, after a refund window, or after a manual review.

For crypto payments, this model is often practical. Buyers can pay in BTC, ETH, USDT, or another supported asset, while the platform keeps seller balances in a more stable accounting currency such as USDT.

The seller balance model also gives the marketplace more control over:

- minimum payout thresholds;

- payout schedules;

- reserves for refunds;

- seller risk levels;

- manual review;

- payout network selection;

- transaction history.

The key requirement is transparency. Sellers should not see only a single balance number. They need a clear ledger of orders, fees, reserves, releases, withdrawals, and adjustments.

What the buyer payment flow should include

The buyer should not see the complexity behind the marketplace. They should see a clear payment request and finish the payment without guessing.

A strong crypto payment flow should show:

- the exact amount;

- the asset;

- the network;

- the payment deadline;

- the payment status;

- what happens after confirmation;

- what to do if the payment fails.

Network clarity matters. “Pay with USDT” is not specific enough. A buyer can send USDT on TRON, Ethereum, BNB Smart Chain, Polygon, or another network. If the invoice expects one network and the buyer sends funds on another, the order may not be detected automatically.

A safer payment instruction is specific: “Pay with USDT TRC-20” or “Pay with USDT on Polygon.” The checkout should also make it clear that the buyer should not manually change the amount.

For marketplaces, small crypto UX errors create a chain reaction. A buyer thinks they paid. A seller waits for an order. Support receives a ticket. Finance later has to investigate the wallet, network, transaction hash, and order status.

This is why network selection, amount accuracy, invoice expiration, QR codes, and payment status updates are not minor details. They are marketplace operations.

How to match crypto payments to marketplace orders

Every crypto payment should be linked to a specific invoice and a specific order. A marketplace should not rely on manual matching by amount, time, and wallet address.

At minimum, the invoice record should include:

- order ID;

- buyer ID;

- seller ID or seller IDs;

- order currency;

- selected crypto asset;

- selected network;

- expected amount;

- invoice expiration time;

- platform fee rule;

- seller allocation rule;

- payment status;

- transaction hash, if available;

- received amount;

- final seller balance entry.

The status model also matters. “Paid” and “not paid” are not enough for a marketplace.

Useful payment statuses include:

- invoice created;

- payment pending;

- transaction detected;

- waiting for network confirmation;

- amount matched;

- underpaid;

- overpaid;

- invoice expired;

- wrong network;

- manual review;

- paid;

- seller balance credited;

- funds available for payout;

- payout requested;

- payout completed.

These statuses reduce confusion. Support can see where the payment stopped. Sellers can see why funds are not yet available. Finance can reconcile expected amounts, received funds, platform fees, reserves, and payouts.

Many failed crypto payments come from the same few issues: wrong network, missing gas, underpayment, expired invoice, or poor checkout UX. These problems are covered in detail in the guide to reducing failed crypto payments. For marketplaces, the same issues need to be tracked not only at the buyer level, but also by seller, category, network, and payment method.

How to handle network fees

Marketplace fees are layered. A single order can involve several types of cost and deduction:

- blockchain network fee;

- payment provider fee;

- platform commission;

- withdrawal fee;

- conversion spread or conversion fee;

- reserve or adjustment;

- category-specific fee.

Problems appear when these are merged into one unexplained deduction. The seller sees less money than expected. The buyer does not understand the exact payment amount. The finance team sees a gap between order value and received funds.

The payment model should separate at least five layers.

First, the buyer amount. This is what the buyer needs to pay for the order to be marked as paid.

Second, the blockchain cost. This depends on the network and can change over time.

Third, the marketplace commission. This is the platform’s revenue.

Fourth, the seller amount. This is the amount credited to the seller after platform deductions.

Fifth, the payout amount. This may differ from the credited amount if there are reserves, payout fees, minimum thresholds, or manual holds.

The marketplace should decide who pays network fees in each situation. Some platforms include the fee in the invoice amount. Some deduct it from the seller. Some absorb it as a cost. Some pass it to the buyer.

There is no universal answer, but the rule must be visible and consistent. A hidden network-fee policy will create disputes.

A good starting point is to understand how crypto network fees work across Bitcoin, Ethereum, TRON, and other networks. Network fees are not just a technical topic. They affect checkout conversion, underpayments, support tickets, and seller trust.

The gas problem in USDT payments

USDT is one of the most common assets for crypto payments, but it comes with a common problem: the buyer may have USDT but not the native token needed to pay the network fee.

For example, a customer may hold USDT on TRON but have no TRX for gas. Or they may hold USDT on Ethereum but have no ETH. The result is frustrating: the customer has enough USDT for the purchase but still cannot complete the transaction.

On a marketplace, this creates operational noise:

- the buyer cannot finish payment;

- the seller does not receive the order status;

- support has to explain gas;

- finance may later review incomplete or delayed payments;

- the marketplace loses trust on both sides.

The article on gasless USDT payments explains why this happens and how businesses can reduce failed payments caused by missing TRX, ETH, BNB, or another native token.

For marketplace design, the lesson is simple: do not assume buyers understand blockchain fees. The payment flow should reduce manual decisions wherever possible.

How to protect seller balances from volatility

If a marketplace accepts BTC, ETH, SOL, BNB, or other volatile assets, it has to decide how to calculate seller balances.

Imagine a product is priced at $100. The buyer pays in BTC. The market moves before the transaction is confirmed. What should the seller receive? What should the marketplace keep as commission? Who takes the price risk?

A marketplace should define:

- when the exchange rate is fixed;

- which currency is used for the order;

- which currency is used for seller balances;

- which asset the seller can withdraw;

- what happens if payment is late;

- how partial payments are valued;

- how conversion appears in reports.

For many marketplace models, stablecoin settlement is easier to operate. Buyers may pay with different assets, while the platform keeps internal balances in USDT or another stable settlement asset. This makes seller statements, platform fees, reserves, and payouts easier to understand.

This does not remove every risk. Conversion depends on provider rules, liquidity, timing, and supported assets. But it gives the marketplace a cleaner accounting layer than holding every seller balance in a volatile asset.

The broader volatility issue is covered in the guide to protecting crypto funds from market volatility.

What sellers should see in their balance

A seller balance is not just a number. It is the seller’s trust interface.

Sellers should be able to answer basic questions without contacting support:

- Which order generated this balance entry?

- When was the buyer payment confirmed?

- Which asset did the buyer use?

- What was the order value?

- What fee did the marketplace keep?

- Was any amount reserved?

- When will the funds become available?

- What amount can be withdrawn now?

- Which payout address was used?

- What is the status of the withdrawal?

A useful seller ledger should separate:

- credited balance;

- pending balance;

- available balance;

- reserved balance;

- withdrawn funds;

- refunded funds;

- disputed funds;

- manual adjustments.

This is especially important when buyers can pay in several crypto assets, but sellers receive balances in USDT. Sellers need to understand that the buyer may have paid in BTC or ETH while the platform credited the seller in a stable settlement currency according to platform rules.

The goal is not to expose every blockchain detail. The goal is to make the money trail understandable.

How to design seller payouts

Seller payouts are one of the most sensitive parts of marketplace crypto payments. The buyer has already paid. The seller expects to receive funds. The platform must protect itself against fraud, disputes, refund windows, wrong addresses, and compliance issues.

Before launch, define payout rules clearly:

- which sellers are eligible for crypto payouts;

- which assets are supported for payouts;

- which networks are supported;

- whether sellers can choose the payout network;

- minimum payout amount;

- payout schedule;

- payout fee policy;

- automatic vs manual payouts;

- payout limits for new sellers;

- payout holds after high-risk orders;

- address change rules;

- two-factor authentication for payout changes;

- what happens during disputes;

- how failed payouts are handled.

New sellers often need stricter rules: manual review, lower limits, longer holds, or reserves. Trusted sellers with clean history may qualify for faster or automated payouts.

For global platforms, stablecoin payouts can be useful where bank transfers are slow, expensive, or hard to access. But payout design should not be reduced to “send USDT.” The platform still needs seller verification, payout logs, address controls, fee rules, and dispute procedures.

The comparison of crypto payments vs bank transfers can support this decision for CFOs and founders evaluating cross-border settlement trade-offs.

AML, KYC, KYB, and seller risk

Marketplaces face a different risk profile than single-merchant stores. They do not only accept payments from buyers. They also route value to sellers.

This means the marketplace should think about both incoming and outgoing risk:

- Who is allowed to sell?

- Which seller categories are prohibited?

- Which buyers or sellers require extra checks?

- Which transaction amounts trigger review?

- Which wallet addresses are blocked?

- What happens if a transaction is flagged?

- Who can approve a blocked payout?

- How is the decision recorded?

- What data must be stored for audits?

Depending on jurisdiction, product category, transaction volume, and marketplace role, KYC or KYB checks may be required for sellers. AML screening may be needed for incoming payments, outgoing payouts, or both. This is not universal legal advice; requirements depend on the marketplace’s structure and operating countries.

From a product perspective, the platform should build the workflow before volume grows:

- seller onboarding;

- risk levels;

- payout limits;

- manual review queues;

- audit trail;

- two-factor authentication;

- role-based admin access;

- suspicious activity handling.

The guide to secure crypto payments, AML, and KYC is a useful internal link for teams building this risk layer.

Refunds and disputes

Crypto transactions are not reversed like card payments. That reduces the risk of classic chargebacks, but it does not eliminate refunds or disputes.

Marketplaces still need rules for:

- canceled orders;

- partial refunds;

- multi-seller orders;

- returned goods;

- failed delivery;

- service disputes;

- duplicate payments;

- overpayments;

- underpayments;

- buyer mistakes;

- seller misconduct.

The hardest case is often a partial refund in a multi-seller order.

Suppose a buyer orders from three sellers in one checkout. One seller cancels. Two sellers fulfill. The platform cannot simply “reverse the payment.” It needs to calculate the refund amount, adjust the canceled seller’s balance, keep or reverse the relevant platform fee, release the remaining sellers’ funds, and record the whole event.

For digital goods, subscriptions, services, and creator platforms, a temporary hold can help. The seller balance is credited after payment, but funds become withdrawable only after a delivery confirmation, acceptance event, refund window, or risk check.

Refund rules should be clear before the first crypto payment goes live. Otherwise, every dispute becomes a custom finance operation.

What the CTO and developers need to plan

A marketplace crypto integration should start with data design, not a payment button.

The engineering team needs to model:

- orders;

- invoices;

- payment events;

- seller allocations;

- platform fees;

- balance entries;

- reserves;

- payouts;

- refunds;

- manual reviews;

- admin actions;

- webhook retries;

- audit logs.

Payment callbacks or webhooks should be idempotent. If the same payment event is received twice, the platform must not credit the seller twice.

The integration should also handle exceptions:

- payment sent after invoice expiration;

- partial payment;

- overpayment;

- wrong network;

- delayed confirmation;

- payment detected but not finalized;

- seller payout address changed;

- AML review required;

- payout rejected;

- refund requested after seller balance was credited.

Each exception needs a status, a support message, and an admin action. Without that, the team will solve payment problems through screenshots, manual wallet checks, and database edits. That does not scale.

A marketplace should also separate buyer-facing and seller-facing states. The buyer may see “Payment received, waiting for confirmation.” The seller may see “Order paid, funds pending release.” Finance may see “Transaction detected, awaiting reconciliation.” These are different views of the same event.

What the CFO should reconcile

Crypto payment reconciliation for a marketplace is not only about confirming that money arrived. It is about proving that each financial event has the right business meaning.

The finance team should reconcile:

- expected order amount;

- actual received amount;

- asset and network;

- exchange rate used;

- platform fee;

- provider fee;

- network fee;

- seller allocation;

- balance entry;

- reserve;

- refund;

- payout request;

- payout transaction;

- final seller statement.

For high-volume marketplaces, manual reconciliation becomes a bottleneck quickly. Every unsupported exception creates extra work: late payment, wrong network, underpayment, overpayment, missing memo, or a seller payout dispute.

The article on stablecoin payment operations for CFOs goes deeper into USDT settlement, fees, conversion, withdrawals, reporting, and risk controls. For marketplaces, the same principles apply, but with an extra seller layer.

Metrics to track after launch

Do not judge crypto payments only by total volume. A marketplace should measure whether crypto payments improve the payment experience without increasing operational noise.

Track these metrics:

- share of orders paid with crypto;

- share of USDT among crypto payments;

- payment success rate;

- underpayment rate;

- overpayment rate;

- wrong-network rate;

- invoice expiration rate;

- average time from invoice creation to payment detection;

- average time from detection to confirmation;

- support tickets per 1,000 crypto payments;

- manual review rate;

- seller balance correction rate;

- average time from paid order to seller credit;

- average time from seller payout request to payout completion;

- refund rate;

- disputed crypto order rate;

- AML review rate;

- payout rejection rate.

These metrics tell the platform where the payment process is breaking. If volume is growing but support tickets and manual corrections are growing faster, the marketplace has not solved the payment problem. It has only moved it from checkout to operations.

Where CryptumPay fits

A marketplace does not need crypto payments as a badge. It needs a payment process that reduces manual errors and connects payments to business operations.

CryptumPay can be relevant for marketplaces that want to accept crypto payments on a website, in an app, in a Telegram bot, or on another digital platform. For marketplace use cases, the practical value is in several layers: QR/app payment flow, network-fee handling, USDT conversion, personal account, withdrawals, AML checks, 2FA, API, and HTML widget integration.

The important point is not to treat these as isolated features. A marketplace needs them to support a full operating flow:

- buyer pays with fewer manual steps;

- the platform receives a clear payment status;

- finance sees the transaction history;

- seller balances can be managed more predictably;

- withdrawals are controlled;

- risk checks are part of the process.

This is especially useful for platforms where buyers return often: digital goods marketplaces, gaming marketplaces, creator platforms, paid communities, top-up products, service marketplaces, and Telegram commerce.

Pre-launch checklist for marketplace crypto payments

Before going live, review the operating model.

Payment model:

- choose one account, split payments, or seller balances;

- define who receives customer funds;

- define how seller shares are calculated;

- define the platform commission;

- document refund and dispute rules.

Checkout and invoice:

- link every payment to an order ID;

- link every order to seller IDs;

- show asset, network, amount, and expiration time;

- prevent manual amount mistakes where possible;

- define statuses for late payment, underpayment, overpayment, and wrong network.

Fees and conversion:

- define who pays the network fee;

- separate provider fees from platform fees;

- define when the exchange rate is fixed;

- decide whether seller balances are kept in USDT;

- show fee details in seller statements.

Seller balance:

- separate pending, available, reserved, withdrawn, and disputed funds;

- show order-level balance entries;

- show payout history;

- define minimum payout thresholds;

- define holds and reserves.

Payouts:

- define supported payout assets and networks;

- add seller payout address controls;

- require extra confirmation for address changes;

- define automatic and manual payout rules;

- set limits for new or high-risk sellers.

Risk and security:

- define seller verification requirements;

- add AML review logic;

- use role-based admin access;

- require 2FA for sensitive actions;

- keep an audit trail for manual decisions.

Support:

- prepare buyer-facing explanations for network, gas, invoice expiration, and wrong payments;

- prepare seller-facing explanations for pending balances, reserves, and payout timing;

- give support teams access to payment status, transaction hash, order ID, and seller allocation;

- document escalation rules for manual review.

FAQ

Can a marketplace just accept USDT to one wallet?

Technically, yes, but it is rarely enough for a growing marketplace. One wallet does not solve order matching, seller allocations, platform fees, seller balances, refunds, risk reviews, or payout history. It may work for a small test, but it does not create scalable marketplace payment infrastructure.

What is the best crypto asset for marketplace payments?

For accounting and seller balances, stablecoins such as USDT or USDC are often easier to operate than volatile assets. But the right choice depends on the buyer base, seller geography, average order value, networks supported, and risk policy. Teams should also understand USDT token standards before enabling multiple networks.

Should sellers receive payouts automatically?

Not always. New sellers, high-risk categories, large withdrawals, and recently changed payout addresses may require manual review or payout holds. Automatic payouts are more suitable for trusted sellers with clean history, clear verification, and predictable transaction patterns.

Do marketplaces need KYC or KYB for sellers?

Often, yes, but requirements depend on jurisdiction, product category, transaction volume, marketplace structure, and the role the platform plays in the flow of funds. This should be reviewed with legal and compliance specialists. From a product standpoint, seller verification, payout limits, AML review, and audit logs should be planned early.

How do you know if crypto payments are working for a marketplace?

Look beyond payment volume. Track payment success rate, failed payment reasons, support tickets, reconciliation time, seller balance corrections, payout speed, refund rate, and manual review rate. If crypto volume grows but finance and support become overloaded, the payment flow needs better automation and clearer statuses.

Conclusion

Crypto payments for marketplaces are not just a checkout option. They are an operating layer between buyers, sellers, and the platform.

To make crypto work, a marketplace must define the full flow: invoice creation, payment detection, network handling, order matching, platform commission, seller balance, reserves, refunds, risk checks, and payouts.

The core question is simple: can the platform clearly answer who paid, for which order, in which asset and network, how much was received, how much belongs to the seller, what the marketplace kept, and when the seller can withdraw?

If those answers are visible in the system, crypto payments can become a useful channel for global marketplace commerce. If those answers require manual wallet checks and spreadsheet reconciliation, the marketplace has not added infrastructure. It has added another source of operational risk.