04.06.2026

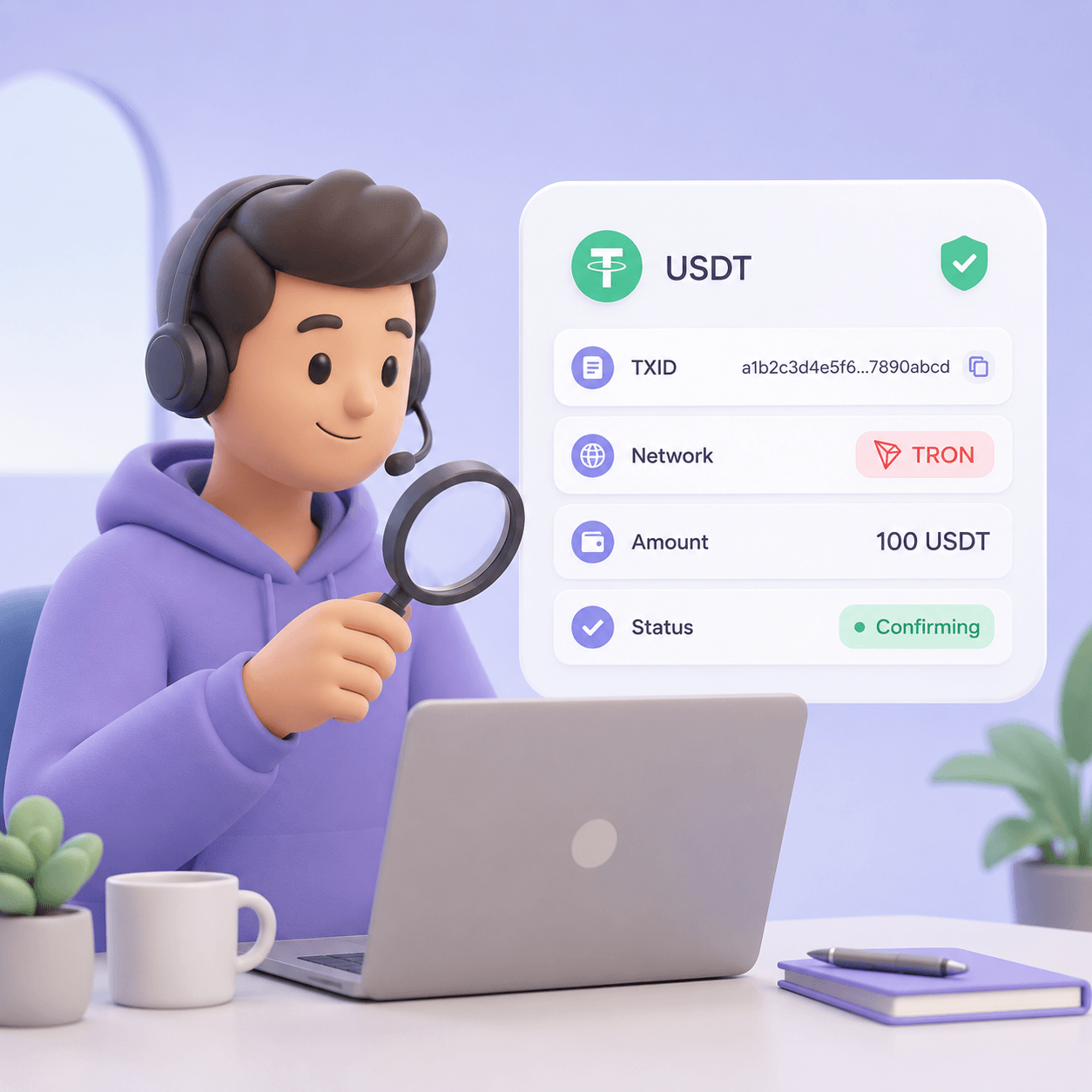

How to Check a Crypto Payment: TXID, Network, Amount, and Status

Read article

Crypto payments are fast, global, and final. That is exactly why businesses need a clear way to review payment risk before a suspicious transaction becomes an operational problem.

A crypto risk score is one of the tools used in that review. It does not prove that a customer is guilty of anything. It is a risk signal based on blockchain data, address history, transaction paths, known entities, and exposure to categories such as scams, stolen funds, sanctioned entities, darknet markets, fraud services, mixers, or other high-risk activity.

For merchants, exchanges, fintech teams, and finance departments, the practical question is simple: when a payment arrives, should it be accepted automatically, reviewed manually, held, refunded, or rejected? This guide explains how AML wallet checks work, what a risk score can and cannot tell you, and how to build a safer payment process.

A crypto risk score is a rating that estimates the risk connected to a wallet address, transaction, or group of addresses. It is usually calculated by blockchain analytics systems that examine on-chain activity and known labels.

The score may be shown as low, medium, or high risk. Some tools use numbers, colors, categories, or alerts. The exact method depends on the provider, but the purpose is usually the same: help teams identify whether a crypto payment needs extra attention.

A risk score may consider:

This is why risk scoring belongs inside a broader payment safety process, not as a standalone verdict. If you are building that process from scratch, start with a broader view of secure crypto payments and AML safety.

An AML wallet check reviews a crypto address or transaction for potential exposure to financial crime risk. In payment operations, this check may happen before accepting a deposit, before releasing a withdrawal, or during manual review of a suspicious transaction.

A typical workflow looks like this:

This process is especially important because blockchain payments are not reversed like card payments. Once funds move to the wrong address or a high-risk flow is accepted without review, the options are limited. For day-to-day payment teams, it helps to combine AML checks with a clear crypto payment check routine.

KYC and wallet screening answer different questions.

KYC checks who the customer is. It may include identity documents, business registration data, sanctions screening, or beneficial ownership checks.

A crypto wallet check reviews where the funds may have come from or where they may go. It looks at blockchain activity, not only customer identity.

A low-risk customer can still send funds from a wallet with suspicious exposure. A high-risk wallet may also require context before a decision is made. That is why regulated and risk-sensitive businesses often combine KYC, transaction monitoring, wallet screening, and internal review.

A wallet may be flagged because it interacted with an address, service, or flow associated with suspicious activity. The most common triggers include sanctions exposure, stolen funds, scams, ransomware, darknet markets, mixers, fraud shops, and high-risk exchanges.

The distance from the source matters. Direct exposure is usually more serious than indirect exposure several hops away. Amount also matters: a tiny dust transaction should not always be treated the same way as a large payment from a known illicit cluster.

Context matters too. A customer may have received funds from an exchange, from a DeFi protocol, from a personal wallet, or from a P2P trade. Some cases are simple. Others require manual review, especially when the user is buying or selling crypto through peer-to-peer channels. For that part of the risk picture, see the guide to P2P crypto scams.

A high-risk score should trigger a defined process. It should not create panic, improvisation, or inconsistent treatment of customers.

A practical policy may include:

Refunds need special care. Returning crypto to the sending address can be risky if the sending address is compromised, sanctioned, or connected to fraud. Before sending funds back, teams should understand their own refund process and the limits of blockchain reversibility. The operational basics are covered in crypto payment refunds.

This article is not legal advice. AML obligations vary by country, license type, customer profile, transaction size, and business model.

Risk scores are useful, but they are not perfect. A wallet can be flagged because of indirect exposure, old activity, dusting, shared infrastructure, exchange activity, or incomplete labels.

That is why a score should be treated as an alert, not a final judgment. A good review process looks at:

The goal is not to block every unusual payment. The goal is to make consistent decisions and reduce preventable risk.

For businesses that accept USDT, USDC, BTC, ETH, or other crypto assets, wallet checks should be part of the payment flow rather than a separate afterthought.

Finance teams should decide when checks happen, who reviews alerts, how long a payment can be held, what support should tell the customer, and how decisions are documented. This is especially important for companies handling larger stablecoin volumes. If your finance team is building those workflows, the guide to stablecoin payment operations is a useful next step.

For businesses that move between fiat and crypto, risk checks also affect on-ramp and off-ramp decisions. Screening is not only about incoming payments; it can also matter before payouts, settlements, and conversions. See the overview of crypto on-ramp and off-ramp flows.

Manual checks can work for occasional transactions, but they do not scale well. Once payment volume grows, businesses usually need API-based screening.

An API can check addresses and transactions automatically, route alerts to the right team, and attach risk data to the payment record. This helps create a consistent process instead of relying on screenshots, manual copy-paste, or individual judgment.

A payment API should make it clear which payment was checked, which address was involved, what the result was, and what action was taken. If you are comparing providers or designing your own flow, use a crypto payment API checklist before implementation.

Risk review should also be measurable. Track how many payments are auto-approved, how many are reviewed, how many are rejected, how long reviews take, and how often customers contact support. These numbers belong next to other crypto payment metrics.

Customers do not always understand why a crypto payment is delayed. The support team should avoid vague or accusatory messages.

Instead of saying that a customer’s wallet is “criminal” or “blocked forever,” use neutral wording:

“We are reviewing this transaction under our payment safety policy. We may ask for additional information before the payment can be completed.”

Good communication reduces confusion and protects the business. It also prevents support agents from making promises that the compliance or finance team cannot keep.

AML expectations continue to evolve. Businesses operating in Europe, for example, need to pay attention to crypto-asset regulation, stablecoin rules, sanctions expectations, and transaction monitoring practices. For a broader business view, read the guide to stablecoin payments in Europe after MiCA.

Even when a company is not a regulated exchange, payment risk still matters. Merchants can face operational losses, frozen funds, reputational damage, or account closures if they repeatedly accept funds from suspicious sources without a process.

Before accepting crypto payments at scale, define:

A good AML wallet check process is not just a tool. It is a policy, workflow, recordkeeping habit, and customer communication standard working together.

No. A risk score is a signal based on available blockchain data and risk labels. It should support review, not replace judgment, policy, or legal advice.

Not always. Some high-risk alerts require rejection, but others need context. The right action depends on the category, exposure level, amount, jurisdiction, customer profile, and internal policy.

Yes. A low-risk result means the tool did not identify meaningful exposure at the time of checking. It does not guarantee that the payment is risk-free.

No. Exchanges, payment providers, fintech companies, marketplaces, and merchants that accept crypto can all benefit from wallet screening, especially when transaction values are high or payment volume grows.

Wallet risk checks review exposure and suspicious activity. They do not replace address verification. Users and businesses still need to protect themselves from fake wallet addresses and address manipulation.

Create an account and connect the checkout yourself, or talk to sales and we will plan the integration with you.

Contact us and we will plan the integration.