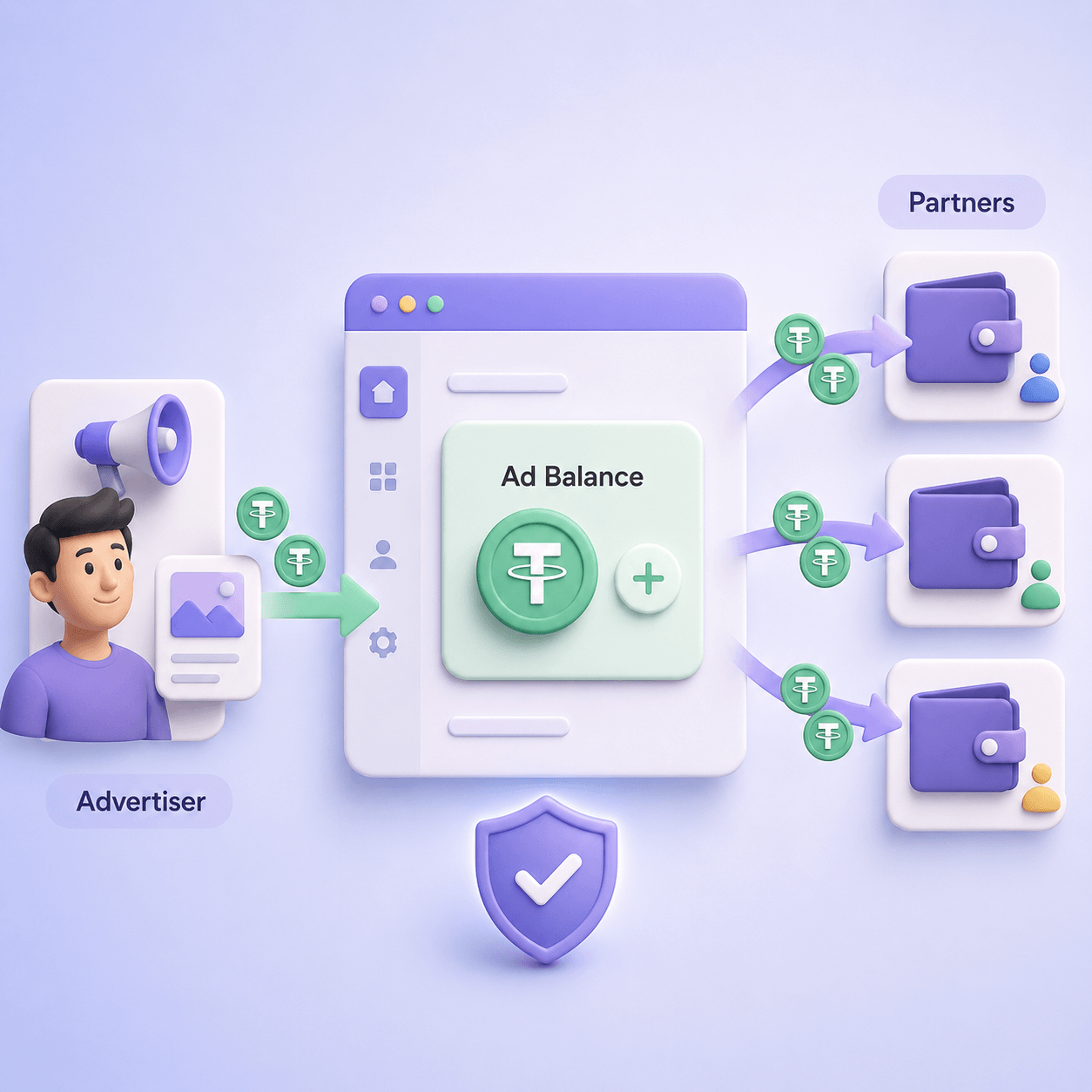

An ad network does not process payments the way a regular online store does. An advertiser is not buying one item and leaving. They fund an account, launch campaigns, increase budgets, test traffic sources, pause underperforming placements, and expect the balance to update without waiting for a manager.

A CPA platform has a second side to manage. It has to calculate commissions, hold questionable conversions, approve partner balances, and pay affiliates, publishers, media buyers, or traffic partners on clear terms.

That is why crypto payments for ad networks are not just a “Pay with USDT” button. They are part of the payment operations behind the platform: advertiser deposits, internal balances, campaign budgets, reconciliation, payout rules, risk checks, and support workflows.

When this logic is not designed properly, crypto quickly becomes manual work. An advertiser sends USDT on the wrong network. A deposit arrives without an account ID. The amount is lower than expected because of a network fee. A partner changes a payout wallet right before a large withdrawal. Finance sees blockchain transactions but cannot match them to campaigns.

The result is familiar: the platform technically accepts crypto, but every edge case lands on support, finance, or developers.

Why ad networks need a different crypto payment model

In e-commerce, payment is usually connected to an order. In SaaS, it may be connected to a subscription or a top-up. In hosting, payments often fund an internal balance that is consumed over time.

Ad networks and CPA platforms combine several models at once. Advertisers deposit funds. Campaign budgets are spent gradually. CPA commissions may depend on approved leads, deposits, sales, or other actions. Affiliates and publishers receive payouts only after the platform applies rules, holds, and adjustments.

So the payment system has to answer more than “Was the invoice paid?”

It needs to know:

- which advertiser made the deposit;

- which account or workspace should receive the funds;

- whether the deposit is linked to a specific campaign;

- which currency and network were used;

- what amount should be credited after fees;

- whether the payment can be credited automatically;

- whether the transaction should be reviewed;

- which partner balances are available for payout;

- which payout requests need approval.

A shared wallet address and manual spreadsheet can work at very low volume. It breaks down once deposits become frequent, advertisers operate across time zones, and partners expect reliable payout schedules.

Two money flows: advertiser deposits and affiliate payouts

Ad networks and CPA platforms usually have two separate money flows.

The first flow is inbound: advertisers fund their accounts. They may use USDT to add budget, prepay campaigns, test a traffic source, or keep an always-on balance for media buying.

The second flow is outbound: the platform pays partners. These can be affiliates, publishers, webmasters, media buyers, channel owners, influencers, or traffic suppliers.

Both flows may use stablecoins, but they are not the same process.

For deposits, the main priorities are speed, account matching, payment status, and automatic balance crediting. For payouts, the priorities are approved earnings, hold periods, minimum payout thresholds, wallet verification, fees, payout history, and risk controls.

This is where many platforms make a mistake. They add crypto only as a deposit method and leave affiliate payouts manual. Advertisers get a better way to fund campaigns, but finance still spends hours preparing partner payments.

A stronger model treats deposits and payouts as connected parts of the same payment operation.

How USDT advertiser deposits should work

A good USDT deposit flow starts inside the advertiser account, not in a chat with a manager.

The advertiser chooses a top-up amount, selects USDT, chooses a supported network, and receives clear payment instructions. The platform creates a payment request and links it to the advertiser account before any funds are sent.

A clean flow looks like this:

- the advertiser clicks “Add funds”;

- the platform creates a payment request for a specific amount;

- the advertiser selects USDT and the network;

- the payment screen shows the amount, wallet address, QR code, and expiration time;

- the advertiser pays from their wallet;

- the payment provider detects the transaction;

- the platform receives a status update;

- the advertiser balance is credited automatically;

- the dashboard shows the payment status, amount, network, and transaction reference.

The important part is not the wallet address. The important part is attribution. Every deposit must be linked to a real advertiser account, internal payment ID, currency, network, expected amount, received amount, and final status.

If your platform has product logic around balances, campaigns, access, or spending limits, review the crypto payment API checklist before integration. For ad networks, an API is valuable because it connects a blockchain transaction to your own system: advertiser ID, invoice ID, balance update, status, webhook, and finance record.

When a widget is enough and when API control is needed

Not every ad network needs a deep API integration on day one. A smaller platform may start with a simpler payment screen, especially if deposits are reviewed manually and account managers are still involved.

A widget can be useful when the goal is to launch crypto deposits quickly and test demand. It gives advertisers a clear payment interface without forcing the product team to build the entire payment experience from scratch.

But API control becomes important when deposits need to update internal systems automatically.

An ad network will usually need API-level logic if it wants to:

- create a payment for a specific advertiser;

- pass an internal account ID or campaign ID;

- credit balance after confirmation;

- handle expired payment requests;

- detect underpayments and overpayments;

- show payment history inside the advertiser dashboard;

- notify finance when a deposit is confirmed;

- block campaign launch until payment is complete;

- process repeated top-ups without manual review.

For lighter cases, an HTML widget for crypto payments may be enough. For platforms with advertiser balances, campaign budgets, automated top-ups, and partner payouts, the widget should usually be supported by backend logic.

Where crypto deposits fail in ad platforms

Advertisers often fund campaigns when timing matters. A campaign is ready. Creatives are approved. A traffic source is available. A test budget needs to go live now.

A failed deposit is not just a payment issue. It can delay campaign launch, waste a traffic opportunity, and create a support ticket at the worst possible moment.

Common problems include:

- the advertiser selects USDT but sends it on the wrong network;

- the amount received is lower than expected;

- the advertiser edits the amount manually in the wallet;

- the payment request expires before the transaction arrives;

- the advertiser sends funds without an account reference;

- the advertiser has USDT but does not have the native coin needed for gas;

- the platform detects the transaction but does not update the balance correctly.

The gas issue is especially common. A user may have USDT on TRON but no TRX, or USDT on Ethereum but no ETH. From their point of view, they have funds. From the wallet’s point of view, they cannot send the transaction.

For an ad network, this creates friction: an unfinished top-up, a delayed campaign, and a support conversation that should have been avoided. The guide to gasless USDT payments explains why users fail to pay without TRX, ETH, or BNB and how businesses can reduce these errors.

How to reduce support workload

Support teams should not have to explain network selection, gas, invoice expiration, and underpayment on every second deposit.

The payment screen should do that work before the advertiser sends funds.

A strong deposit flow should clearly show:

- the asset, such as USDT;

- the network, such as TRON, Ethereum, BNB Smart Chain, Solana, or Polygon;

- the exact amount to send;

- the payment request expiration time;

- a warning not to change the amount manually;

- the current status after payment;

- a useful message if the payment fails or needs review.

“Pay with USDT” is often too vague. “Pay with USDT on TRON” is clearer. If the platform supports several USDT networks, the user should understand that the network matters before opening a wallet.

It also helps to classify failed payments by reason: wrong network, missing gas, underpayment, expired request, late payment, delayed confirmation, or abandoned payment screen. This gives product and payment teams a practical roadmap for reducing friction. The article on failed crypto payments covers these failure points in more detail.

How to connect payments to accounts, campaigns, and finance

The operational goal is not only to receive USDT. The goal is to credit the right internal balance and keep the records clean.

At minimum, each deposit should include:

- advertiser ID;

- payment request ID;

- expected amount;

- received amount;

- currency;

- network;

- status;

- creation time;

- expiration time;

- transaction hash;

- credited balance amount;

- fee data, if shown separately;

- campaign ID, if the deposit is tied to a campaign;

- metadata for finance or operations.

Without this structure, finance sees incoming blockchain transactions but cannot easily answer business questions: which advertiser paid, which balance changed, whether the campaign can run, what fee was applied, and whether the transaction belongs in a specific reporting period.

This is where ad networks resemble multi-sided platforms. Money comes from one side, while obligations may exist on another side. The article on crypto payments for marketplaces is a useful adjacent reference for reconciliation and payouts, but ad networks need their own logic. Instead of buyer, order, seller, and marketplace fee, they have advertiser, campaign, offer, affiliate, conversion, hold, and payout.

Why USDT is often the default for ad network payments

Advertising budgets are usually planned in dollars or dollar-linked units. That makes USDT convenient for ad networks and CPA platforms: advertisers understand how much they are funding, and finance teams can reconcile balances more easily.

BTC and ETH may still be useful as additional payment options, especially for crypto-native advertisers. But for regular balance top-ups, volatile assets create extra questions. Which exchange rate should be used? Should the platform credit the balance at invoice creation, payment detection, final confirmation, or conversion?

Stablecoins reduce that uncertainty. They do not remove all risk, but they make account balances and payouts easier to understand.

USDT still needs careful handling because it exists across different networks. To a user, it may look like one asset. To a payment system, USDT on TRON, Ethereum, BNB Smart Chain, Polygon, Solana, or another supported network can mean different fees, speeds, wallet behavior, and support cases.

Before launching, review the guide to TRC20, ERC20, BEP20, and other USDT formats. It helps teams explain network choice instead of treating USDT as one simple payment method.

How to think about network fees

Fees matter in advertising. When advertisers deposit frequently and platforms pay many affiliates, small differences in fee rules can affect margin, reporting, and partner satisfaction.

There are several ways to handle fees:

- the platform absorbs the network fee;

- the fee is included in the payment amount;

- the advertiser pays the fee;

- the fee is deducted from partner payouts;

- the fee is handled differently by network;

- high-volume advertisers or partners get custom terms.

The main rule is consistency. Advertisers should know how much will be credited to their account. Affiliates should know how much they will receive. Finance should be able to separate blockchain network fees, payment provider fees, and the platform’s own commercial fees.

The article on crypto network fees is useful for the underlying mechanics. For ad networks, the practical question is how those fees appear in balances, deposits, payout requests, and reports.

Affiliate payouts: what CPA platforms need to control

For a CPA platform, crypto payouts can be just as important as crypto deposits. Affiliates and publishers often work internationally, compare payout terms across networks, and care about speed, minimum thresholds, fees, and reliability.

But an affiliate payout is not just a transfer to a wallet. It has to reflect the platform’s commercial rules.

A CPA platform needs to control:

- commission model: CPA, revenue share, hybrid, fixed fee, or custom deal;

- hold period for leads, sales, or deposits;

- minimum payout amount;

- payout schedule: daily, weekly, Net-7, Net-15, Net-30;

- manual review rules for traffic quality;

- rejected or disputed conversions;

- balance adjustments;

- payout currency;

- payout network;

- partner wallet verification;

- history of wallet changes;

- approval roles for large payouts.

If this logic is not built into the platform, crypto payouts can create disputes. A partner sees one balance in the dashboard, receives another amount on-chain, and asks why the fee was different. A finance manager approves a payout but cannot see that the wallet address was changed the same day. A traffic-quality review changes a partner balance after the payout file was prepared.

Good payout operations need traceability: who requested the payout, which wallet was used, which rules were applied, who approved it, what amount was sent, which fee was deducted, and what the final status is.

How to reduce risk in partner payouts

Ad networks and CPA platforms work with many counterparties: advertisers, affiliates, publishers, agencies, media buyers, influencers, traffic suppliers, and sometimes sub-partners. That makes payout risk a real operational issue.

At a minimum, platforms should consider:

- wallet checks before payouts;

- restrictions on last-minute wallet changes;

- two-factor authentication for financial settings;

- separate roles for requesting, approving, and executing payouts;

- audit logs for balance and wallet changes;

- manual review for unusually large payouts;

- AML checks for suspicious wallet activity;

- jurisdiction-specific requirements for compliance and reporting.

AML and KYC requirements vary by jurisdiction, business model, customer profile, and transaction flow. They should not be treated as a universal checklist that works the same way everywhere. But ad networks should not ignore this layer. Cross-border advertising and affiliate payments can involve high-risk geographies, disputed traffic sources, and counterparties that change wallets frequently.

The article on secure crypto payments, AML, and KYC is a good starting point for the risk layer. For CPA platforms, the key is operational control: wallet history, roles, review rules, limits, logs, and clear escalation paths.

Why repeated deposits matter more than the first payment

A first deposit proves that crypto payments work. Repeated deposits prove that the payment flow supports the business model.

Ad networks make money when advertisers keep funding campaigns. If every top-up requires a new chat, a copied address, a manual check, and a support response, the platform has not solved the real problem.

Track repeated top-up behavior separately:

- how many advertisers make a second deposit;

- how long it takes from starting a top-up to balance credit;

- how many deposits require manual review;

- how many payment requests expire;

- how many deposits are underpaid;

- how many users choose the wrong network;

- how often repeat advertisers contact support.

This is close to the top-up logic used in SaaS and other balance-based products. The article on recurring crypto payments for SaaS covers repeat payments and saved payment flows. For ad networks, the same idea applies to campaign budgets rather than subscriptions.

What advertisers and affiliates should see in the dashboard

A good dashboard reduces support workload and improves trust.

Advertisers should be able to see:

- current balance;

- pending deposits;

- confirmed deposits;

- failed or expired payment requests;

- currency and network;

- credited amount;

- fee, if shown separately;

- transaction reference;

- payment status;

- date and time.

Affiliates need a different view:

- approved earnings;

- pending earnings;

- hold amount;

- rejected or adjusted conversions;

- available payout balance;

- requested payouts;

- completed payouts;

- payout wallet;

- network;

- fee;

- status.

Finance needs a third layer:

- total deposits by period;

- total payouts by period;

- balance changes;

- fees;

- networks used;

- advertiser-level records;

- affiliate-level records;

- exportable reports;

- unresolved transactions;

- transactions under review.

This is where payment data becomes financial infrastructure. The guide to stablecoin payment operations for CFOs explains how USDT payments, fees, reconciliation, conversion, withdrawals, and reporting fit into finance workflows.

When an ad network needs white-label crypto payments

A hosted payment screen can be enough for a simple launch. But larger ad networks and CPA platforms often need the payment experience to feel like part of their own product.

White label becomes relevant when:

- high-value advertisers fund accounts regularly;

- the payment flow sits inside a branded advertiser dashboard;

- affiliates manage payout settings in a partner cabinet;

- the platform wants fewer redirects to third-party-looking pages;

- account managers need a consistent experience for clients;

- reporting and payment status must match the platform’s own interface;

- the business wants more control over the payment journey.

This is not just a design issue. It affects trust. Advertisers funding campaigns want to know they are still inside the platform they use to run traffic. Affiliates requesting payouts want clear status updates and familiar account controls.

The white-label crypto payment gateway article is written for PSPs, but many of the same questions apply to ad networks: branding, API depth, payment statuses, AML checks, reporting, settlement, and support workflows.

Where CryptumPay can fit

CryptumPay can be considered by businesses that need to accept crypto payments on a website, app, Telegram bot, or another digital platform. For ad networks and CPA platforms, the useful part is not one isolated feature. It is the combination of payment flow, API or HTML widget, supported assets and networks, payment statuses, dashboard visibility, AML checks, withdrawals, and automatic conversion to USDT.

For advertiser deposits, this can help the platform move away from manual wallet transfers and toward structured payment requests connected to advertiser accounts. For partner payouts, it can support a more controlled operating model around wallet data, transaction history, fees, and internal approval rules.

CryptumPay also addresses some fee-related friction in crypto payments. In specific scenarios, the payment logic can account for network fees and help users complete payments without manually solving the native-token problem every time. For an ad network, this matters because a failed deposit can delay a campaign, not just interrupt a checkout.

What to check before integration

Before adding crypto payments to an ad network or CPA platform, do not start with the question “Can we accept USDT?” Start with the full operating chain.

For advertiser deposits, check whether the provider supports:

- payment requests tied to advertiser accounts;

- metadata for account ID or campaign ID;

- USDT across the networks your users actually need;

- payment statuses for detected, confirmed, expired, underpaid, and overpaid transactions;

- server-side notifications;

- automatic balance crediting;

- clear handling of late payments;

- reporting for finance.

For affiliate payouts, check whether your platform can manage:

- verified payout wallets;

- payout approval rules;

- hold periods;

- minimum payout amounts;

- network fee visibility;

- payout history;

- balance adjustments;

- manual review for risky payouts;

- role-based access.

For security and compliance, check:

- two-factor authentication;

- role separation;

- audit logs;

- AML screening;

- suspicious transaction handling;

- wallet change history;

- access controls for financial settings;

- jurisdiction-specific requirements.

This prevents the project from becoming “we added USDT to the payment page.” For an ad network, crypto payments only work well when they connect to balances, campaigns, partner earnings, finance reports, and risk controls.

Crypto payments are payment operations, not just a payment method

Crypto payments for ad networks and CPA platforms are most useful when they are built into the business model.

Advertisers need a fast way to fund accounts. The platform needs to credit the right balance. Finance needs clean reconciliation. Affiliates need predictable payouts. Support needs fewer manual investigations. Risk teams need visibility into wallets, roles, and unusual activity.

USDT and other cryptocurrencies can make international advertising payments more flexible, but they do not solve operational problems by themselves. The real value comes from the infrastructure around them: payment requests, statuses, API events, fee logic, network handling, AML checks, dashboards, and payout controls.

For an ad network, “we accept crypto” is not the end goal. The goal is better payment operations: advertisers can top up faster, campaigns do not wait for manual reconciliation, and affiliates receive payouts under clear rules.